What exactly is the “seven-year rule” for Inheritance Tax, and how does it work?

The government’s Autumn Budget is fast approaching on 26 November, and Inheritance Tax (IHT) could well be among the measures the chancellor targets to raise tax revenues.

Last year, the government announced plans to include pensions within the IHT net from April 2027. This year, we may see similar changes to the tax, or none at all.

Until we know exactly what will be in the Budget announcement, our recommendation at Caliber is to keep calm, carry on, and don’t react until you have the facts you need to make informed decisions.

Read more: Why it’s important to stay calm ahead of Budget uncertainty

All this discussion around IHT reminded us of an article we wrote last year exploring tax-efficient gifting. In it, we looked at some of the ways you can give money to your loved ones while reducing your IHT liability. We explained three ways you can do this:

- Using your annual gifting exemption (£3,000 in 2025/26).

- Making potentially exempt transfers.

- Gifting wealth from surplus income.

At the time of writing, all three methods remain effective ways to make tax-efficient gifts to your family. That could change at the Budget on 26 November.

In the meantime, you may still want to consider using these allowances and exemptions to reduce the IHT bill that could be due on your estate.

But before you do, it’s worth being aware that the second of these rules – potentially exempt transfers, or “PETs” – is often misunderstood.

Otherwise known as the “seven-year rule”, this tax break theoretically allows you to make unlimited gifts to whoever you’d like without the recipient facing an IHT charge. The main caveat is that you must survive the gift by seven years or more for there to be no tax bill. If you die within that period, tax may be due.

That’s the basic principle of the rule. However, as with many financial regulations, it’s actually slightly more complicated than this.

So, discover how the seven-year rule works, some of the complexities to be aware of, and how a financial planner can help you organise your estate so it’s as tax-efficient as possible.

Gifts are tax-free after 7 years, and the tax rate could taper if you die in the meantime

The seven-year rule works differently from most other IHT-efficient gifting exemptions and allowances.

As explained above, it dictates that gifts you make and then survive for seven years will fall outside your estate for IHT purposes. At that point, the PET is considered successful, and no tax will be due upon your death.

Meanwhile, if you die within those seven years after making the gift, it becomes a “failed PET”. This gift could then become subject to tax – hence the “potentially exempt” element of the PETs acronym.

However, rather than facing the standard 40% IHT charge, your beneficiaries may pay a variable amount depending on the timing of the gift. That’s because PETs may be able to benefit from taper relief.

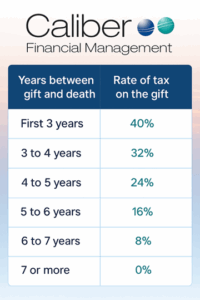

Depending on how many years have passed between you making the gift and dying, the rate of IHT due on the gift may be tapered. The table below shows the rate of IHT payable when taper relief is applied:

As this table shows, the potential tax savings from taper relief could be significant. Even if you don’t survive the full seven years, you can see how PETs could be a useful part of your financial planning.

Potentially exempt transfers will be the first part of your estate assessed against your nil-rate band

Before you start making PETs to give your beneficiaries a better chance of benefiting from a lower rate of IHT, there’s one more caveat about taper relief that you need to understand.

Before IHT is due, every individual has a nil-rate band that allows them to pass on money and assets in their estate tax-free to their beneficiaries. In 2025/26, this threshold stands at £325,000.

Your beneficiaries may also be able to claim the additional residence nil-rate band of up to £175,000 (2025/26) if you leave your main residence to a direct descendant, such as a child or grandchild.

The nil-rate band is very important to PETs and the potential tax they may incur. That’s because, when it comes to calculating your estate and any associated tax bill, any PETs you made will be the first element assessed against your nil-rate band.

If you have sufficient remaining nil-rate band and your PETs do not exceed it, then your beneficiaries won’t benefit from taper relief. Instead, the gift will be tax-free, using up that part of your nil-rate band.

Consider this example. You make a PET of £100,000 to your child and then die three years and six months later. You have a total remaining estate of £500,000 and still have your entire £325,000 nil-rate band. You do not own your home and so cannot benefit from the residence nil-rate band.

Instead of that £100,000 facing 32% tax, it is assessed against your nil-rate band. That means:

- The £100,000 PET is tax-free under the nil-rate band

- Only the first £225,000 of your estate is covered by your remaining nil-rate band

- Assuming you have no other measures in place to mitigate IHT, that leaves £275,000 of your estate subject to IHT

- Your beneficiaries will have to pay a 40% IHT bill on the £275,000 they inherit, leaving them with a £110,000 charge.

With this in mind, it might seem like opportunities to benefit from taper relief are limited. But that’s not necessarily the case.

For example, if you make PETs in excess of £325,000 (or £500,000 if your beneficiaries can claim the residence nil-rate band), the sums above this amount could benefit from a reduced rate of IHT if you die within seven years.

Similarly, you may use some of your nil-rate band when placing assets in trust. Then, any failed PETs you make could also be eligible for taper relief.

So, while these rules may reduce the likelihood of it happening, there are still times when your beneficiaries could face a lower IHT rate on your gifts.

A financial planner can help you tax-efficiently organise your estate

As you can see, the seven-year rule is complex and comes with key caveats that you need to keep in mind before gifting.

This is where working with a financial planner can be helpful. At Caliber, we can support you in making your estate as tax-efficient as possible, explaining the impact of rules like this and assisting you with gifts that mitigate IHT as far as possible.

Beyond gifting, we might make other recommendations for your wealth that could improve your estate’s tax efficiency. From choosing beneficiaries tactically to trust planning, we can help you understand your options.

If you’d like to speak to an experienced financial planner about tax-efficient estate planning, please do get in touch today.

Email contact@caliberfm.co.uk or call 01525 375286 to speak to one of our team.

Please note

This article is for general information only and does not constitute advice. The information is aimed at retail clients only.

All information is correct at the time of writing and is subject to change in the future.

Please do not act based on anything you might read in this article. All contents are based on our understanding of HMRC legislation, which is subject to change.

The Financial Conduct Authority does not regulate estate planning, tax planning, or will writing.

Remember that taper relief only applies to gifts in excess of the nil-rate band. It follows that, if no tax is payable on the transfer because it does not exceed the nil-rate band (after cumulation), there can be no relief.

Taper relief does not reduce the value transferred; it reduces the tax payable as a consequence of that transfer.